|

U.S. Attorneys' Office Thanks Ticor

By Lisa A. Tyler

National Escrow Administrator

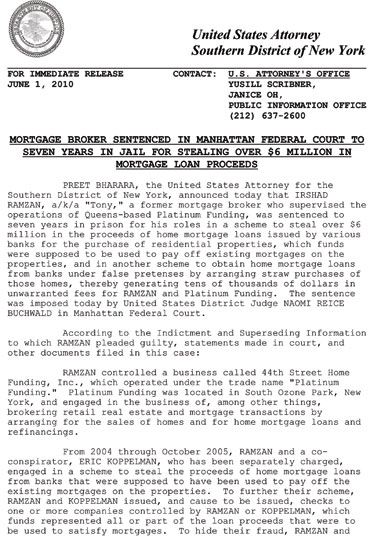

In a press release dated June 1, 2010 Preet Bharara, the U.S. Attorney for the Southern District of New York, publicly thanked Ticor Title Insurance Company for its assistance in an ongoing investigation. Ticor provided the assistance needed to prosecute and sentence Irshad Ramzan a former mortgage broker who had supervised the operation of Platinum Funding. As a result of the investigation and conviction, Ramzan was sentenced to seven years in prison for his role in a scheme to steal more than $6 million in proceeds of home mortgage loans issued by various banks. Learn more about the crimes committed by Ramzan and his co-conspirators in this edition of Fraud Insights.

It's hard enough for settlement agents to clean up their own dead inventory and dormant funds. Can you imagine performing that job for multiple agents in multiple offices? What a tremendous and tedious job. In this edition of Fraud Insights, we share with you a story about a post-closing department that does just that – cleans up dormant funds from closed offices. In the story entitled "Closed Office Cleanup" readers will learn how a real estate agent tried to dupe our post-closing department manager and an unsuspecting buyer out of $5,000.

Here's a new twist on an old trick! We've reported the same sort of counterfeit check scheme in three previous editions of Fraud Insights – the Dec. 2009, May 2010 and June 2010 editions. The common theme in each article involved counterfeit checks drawn on Canadian banks. Each article instructed the receiving offices not to deposit checks drawn on a foreign bank for any reason due to increased processing time and fees charged by the banks. The fraudsters must have read the articles, because their latest trick is to send counterfeit checks drawn from U.S. banks and credit unions. Read about the latest incident in the story entitled "If It Happens In Whitefish…It Can Happen Anywhere!"

|

|

|

|

|

U.S. Attorneys' Office Thanks Ticor

Irshad Ramzan, a mortgage broker, together with Eric Koppelman, a title agent, pilfered $6 million in funds received from lenders that were supposed to be used to pay off loans between 2004 and 2005. Instead the two criminals wrote checks to companies they controlled. Both men were prosecuted by the U.S. Attorneys' Office and Ticor was instrumental in bringing the two to justice.

Ramzan controlled a business mortgage brokerage named Platinum Funding in New York. Koppelman was a former executive with Aegis America, a Manhattan Title Agent who was underwritten by Ticor Title Insurance. The two men engaged in a scheme to steal the proceeds of home mortgage loans from banks that were supposed to have been used to pay off the existing mortgages and taxes on the properties. They stole more than $6 million from 15 insured lenders on 33 different loans.

To hide their fraud, Ramzan and Koppelman lied to the banks providing the loans and directed the loan proceeds to companies they each controlled. In addition to stealing the loan proceeds, Ramzan and Koppelman collected tens of thousands of dollars in unwarranted fees through their transactions as the mortgage broker and title agent. Their crimes were reported to the U.S. Attorneys' Office.

Ticor stepped in to provide key facts in the case that assisted in the prosecution of Ramzan and Koppelman. In addition to the seven-year prison entence, Ramzan was sentenced to four years of supervised release, ordered to pay $6 million in restitution and, as a result, forced to forfeit several of his properties. Koppelman plead guilty to conspiracy to commit bank fraud, but has not yet been sentenced.

The U.S. Attorneys' office issued a press release regarding the conviction and sentencing and in it thanked Ticor for its assistance in the investigation. View the full press release at the link provided below: ramzanirshadsentencingpr.pdf

|

|

Closed Office Cleanup

A post-closing department employee took the initial step to disburse a $5,000 deposit on a very old sale transaction, sending out mutual cancellation instructions to the principals and their agent. The principals immediately agreed on the release of funds to the buyer and returned mutual instructions to the post-closing department. Surprisingly, the real estate agent did not agree to the release of funds to the buyer.

It's no secret that as a result of a downturn in the economy, the Company has elected to close offices. Part of the process for closing down an existing office includes the disbursement of all funds in the escrow trust account until it is at a zero balance. Funds held on active files are moved to the offices taking over the existing inventory. Inactive files with a balance are considered dormant and are sent to the post-closing department to clean up and disburse funds to the rightful owner. The Company has established several post-closing departments throughout the country to clean up the trust accounts of closed offices.

One such department is headed by Sharla Rush in Northern California. Sharla and her associate, Marilynne McDuffey, were cleaning up dormant funds for a closed Commonwealth Land Title office. Marilynne found a file with a $5,000 deposit. From the notes in the file it appeared the buyer failed to qualify for new financing, which was a contingency of the contract. Marilynne sent out mutual cancellation instructions to the principals and their agent.

The principals returned the mutual instructions releasing the $5,000 to the buyer. However, the real estate agent, who was also a broker and represented both sides of the transaction, sent in a written demand to the post-closing department for the $5,000, indicating he had refunded the buyer himself because he heard Commonwealth went out of business. Marilynne escalated the file to Sharla, the department manager.

Marilynne and Sharla were concerned because it seemed the buyer was expecting a refund which the real estate agent claimed was already received. Sharla called the buyer, who clearly did not recall receiving a refund of his $5,000 earnest money deposit. Next Sharla called the real estate agent. Sharla requested a copy of the front and back of the paid check to prove to the buyer he had already received a refund, so she could reimburse the real estate agent these funds.

The real estate agent sent Sharla a copy of the front and back of the cancelled check. Sharla contacted the buyer again stating she had a copy of the cancelled check proving he must have already received the refund of his deposit. The buyer still insisted he did not receive payment. Sharla contacted the issuing bank on the cancelled check to confirm the check was valid and negotiated. The banking contact revealed the check copy provided to Sharla did not match the bank records and was in fact never paid – it was a copy of a counterfeit check!

After this discovery, Sharla attempted numerous calls and letters to the real estate agent – none of which have ever been returned. She ultimately released the funds back to the buyer.

If Sharla and Marilynne had refunded the $5,000 to the real estate agent, the Company might have received a claim from the buyer for his loss. For their efforts in protecting the Company from a potential claim and for protecting the public we serve, Sharla and Marilynne have split a $1,000 reward and have each received letters of recognition.

|

|

If It Happens In Whitefish…

It Can Happen Anywhere!?

The property had been on the market for more than a year with no offers. Finally the property owner switched listing agents and the property sold for the asking price! The purchase contract had no contingencies and a quick closing date. It sounded too good to be true.

Rena Saunier, the escrow manager for Fidelity's Whitefish, Mont. office, recently opened an all-cash purchase transaction in the amount of $560,000. The purchase contract was a full price offer submitted by an individual in China named Lan Jianhua. Jianhua was not represented by a real estate agent and made the offer through the listing agent site unseen. The listing agent was leery of this offer based on the "too good to be true" factor, however with fingers crossed he opened the order with Rena. The listing agent asked Rena to e-mail Jianhua the wire instructions for where to send the earnest money deposit required by the contract.

Rena e-mailed the buyer with her contact and wire transfer information. A week went by before Rena heard back from Jianhua. He wanted to know if his financial broker had been in contact with her about remitting the funds to purchase the property. Rena responded that she had not received any communications with regard to the transaction, nor had she received the funds. Another week went by and in the mail Rena found a cashier's check in an envelope mailed from Canada. The cashier's check was in the amount of $190,000 drawn on the Indian River Federal Credit Union in Vero Beach, Fla.

Rena looked up the credit union on the Internet and found a telephone number. Rena was concerned the person on the other end of the telephone might be part of the suspected scam, so her conversation must have seemed a bit cryptic. She asked for a manager who could confirm whether or not the cashier's check in her hand was, in fact, real. She was transferred to a manager who was able to confirm the credit union had not issued the cashier's check. The manager proceeded to tell her they had opened a police investigation due to several counterfeit checks that were circulating all over the nation. The manager was very appreciative of Rena's phone call.

When Rena hung up, she sent Jianhua an e-mail to let him know the original check was being mailed to the address provided in the purchase contract in China and that any future deposits would only be accepted in the form of a wire transfer. The buyer wrote back claiming he was shocked and outraged! He said it was not possible the check was counterfeit because he had invested a lot of money with the financial broker who sent the check. He demanded Rena e-mail a copy of the check so he could initiate his own investigation. There was no mention of remitting legitimate funds to consummate the transaction, nor was any concern expressed about the effect this had on the contract close date – shocker!

The following details tipped off Rena the cashier's check might be counterfeit:

- The contract called for a $10,000 deposit – the cashier's check was in the amount of $190,000

- The cashier's check from Vero Beach, Fla. was sent from Canada for a purchaser in China

- The bank address was a post office box

- None of the security features listed on the back of the check were present, including: the warning band, microprint border, "coloured" background on "cheque" and original document security screen

- The words "coloured" and "cheque" were not written in English

In a statement Rena said, "I can honestly say that had I not been pre-warned about this type of fraud, I might have overlooked several of these details. Fraud Insights is a terrific tool and it has saved our operation a potential loss and a lot of extra work by identifying this scenario as a type of fraud. Thank you for providing us with such excellent education in this crazy industry."

For her instinct and diligence, Rena has received a $1,000 reward and a letter of recognition from the Company. Her quick detection of the fraud saved the Company from preparing title reports, processing curative work and preparing statements for which we would never be paid. She also saved the seller valuable market time by identifying the fraud and notifying all parties, enabling the seller to put the house back on the market.

|

|